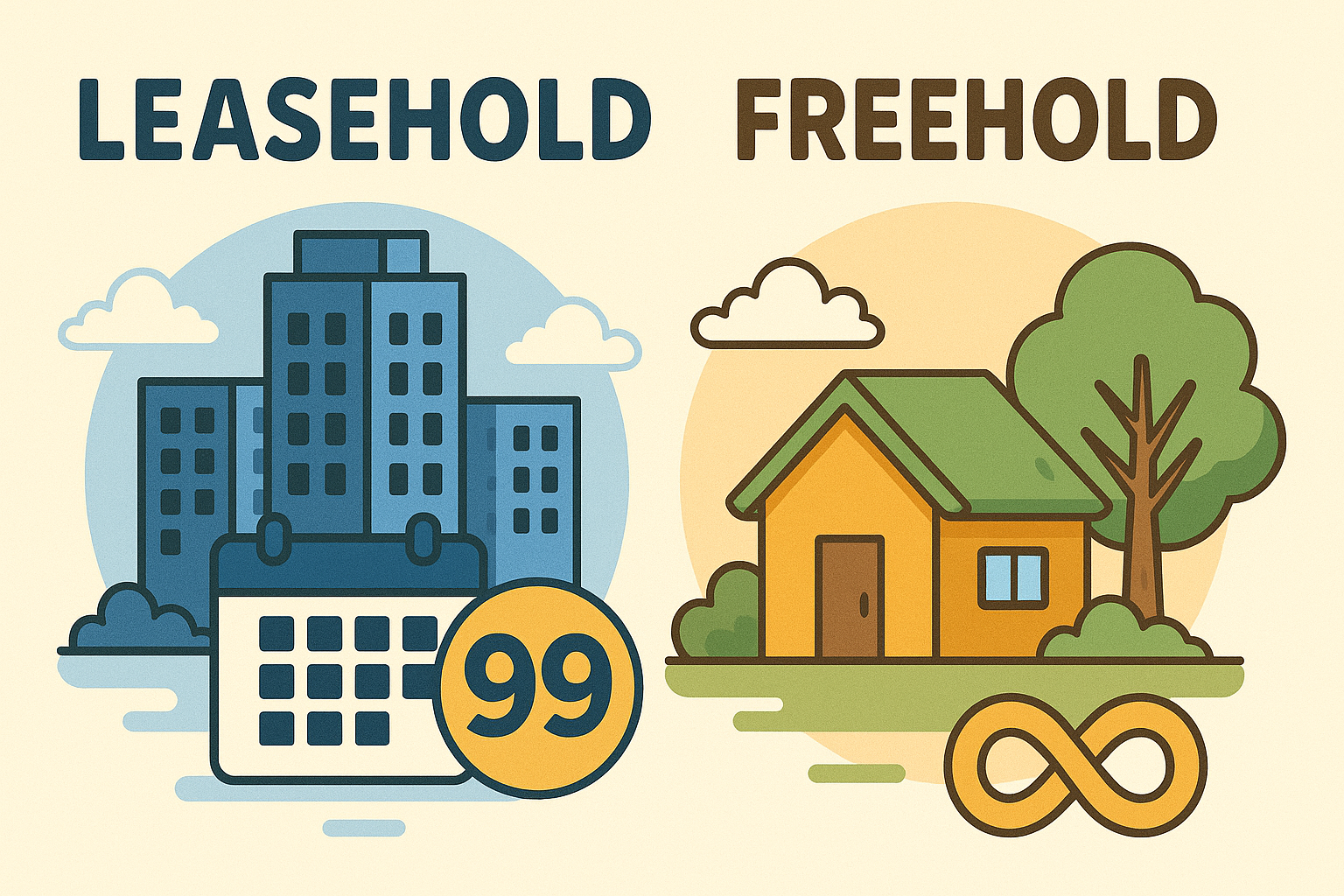

Leasehold vs Freehold: What’s the Difference?

When buying property in Singapore, one of the most common questions is: Should I buy freehold or leasehold?

The physical unit may look exactly the same, but the tenure (length of ownership) makes a big difference in price, value, financing, and long-term planning. Understanding this distinction helps you make a smarter, future-proof decision.

{kind=link}

What is Freehold Property?

A freehold property means you own both the unit and the land beneath it indefinitely. In other words, there’s no expiry date.

Why buyers like freehold:

- Forever yours: It can be passed on from generation to generation without worrying about lease expiry.

- Better value retention: Freehold properties hold their value well compared to leasehold, especially after surrounding projects start ageing.

- Scarcity factor: Only about 20% of private homes in Singapore are freehold. Scarcity often creates higher demand.

Downside: Freehold units usually come with a price premium of 15%–25% compared to leasehold units in the same location. For many buyers, this higher entry cost means either buying a smaller unit or compromising on location.

What is Leasehold Property?

Most properties in Singapore are 99-year leasehold. This means you own the unit for 99 years, after which ownership reverts to the state.

Types of leasehold:

- 99 years: The most common type, especially for HDB flats and new condos.

- 999 years: Almost “as good as freehold” — practically no difference for most buyers.

- Shorter leases: Some projects have leases of 60 years or less (e.g., industrial properties or very old developments).

Why buyers like leasehold:

- More affordable: Lower entry cost makes it attractive for first-time buyers and investors.

- Higher rental yield: Because the purchase price is lower, yields can look more attractive.

- Better locations: Sometimes, a leasehold in a prime location (near MRT or CBD) beats a freehold in a faraway area.

The risk: Lease decay. As the lease drops below 70 years, resale demand weakens, financing gets tougher, and property values usually decline.

Financing Impact: Why Banks Care About Tenure

One major factor often overlooked is loan eligibility. Banks consider remaining lease when approving loans:

- If the lease covers the buyer up to age 95: ✅ full financing allowed (up to 75% for first property).

- If lease is too short: ❌ loan quantum reduced, which means you need more cash upfront.

For example, buying a 40-year-old leasehold condo with 59 years left may only get you a smaller loan amount. That’s why older leasehold units often have fewer buyers.

Case Study: Same Condo, Different Tenure

Imagine two condos side by side in the same neighbourhood:

- Freehold condo unit: $1.5M

- 99-year leasehold condo unit: $1.2M

At first glance, the leasehold is cheaper and gives higher rental yield. But fast-forward 30 years — when the leasehold unit has only 69 years left, its value may stagnate or fall, while the freehold still holds demand.

This doesn’t mean freehold is always better — it depends on whether your priority is short-term returns or long-term security.

Which Should You Choose?

The “better” option depends on your life stage, goals, and financial strategy:

- For investors: Leasehold makes sense because of the lower entry price and potentially higher yields. You can sell before lease decay becomes an issue.

- For families/legacy planning: Freehold offers peace of mind if you intend to keep the home for generations.

For practical buyers: Sometimes, location outweighs tenure. A leasehold near MRT or a top school may outperform a freehold that’s far away.

Key Takeaway

Freehold properties are like long-term security blankets — expensive, but forever yours. Leasehold properties are like practical workhorses — affordable, flexible, but with an expiry date.

👉 The smart choice is not about which is “better” in general, but which aligns with your goals, budget, and timeline.