Alot of readers/clients were asking me. “Derek, now there are talks about Recession, higher interest rate, wars /tensions, will we see a drastic drop in private property price?”

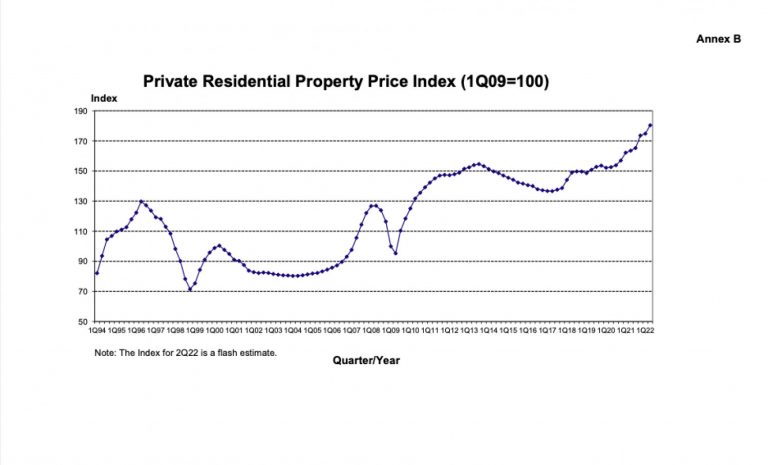

Two of the world’s major financial crisis happened in 1997 (Asian Financial Crisis) and 2009 (Subprime crisis). If we used the Private Residential Property Price Index (PPI) by URA, we see a dropped of 60 index point or about 45% in 1997 and 40 index point or about 30% in 2009. While the world has changed from then to now, so has policies and differences in the scenarios then and now. Here are some reasons why I felt we are unlikely to see a drastic drop as compared to previously in Singapore.

The introduction of Total Debt Servicing Ratio

In 2013, The Monetary Authority of Singapore (MAS) introduced the above framework when any loans (property, auto, personal, study, credit etc) given by financial institutions are capped at 60% of any borrower’s income. This was then revised to 55% in 2021. What it essentially does is to ensure that there is a level of prudency when taking up loans to acquire properties as compared to the past. Coupled with the introduction of Additional Buyer Stamp Duty (ABSD) these greatly reduced the possibilities of structural distressed sellers that we see in 1997 and 2009.

Relatively strong GDP & Economy diversification

Singapore has divested its economy (including potentially recession-proof sectors) and have recovered relatively well from the pandemic. Of course, as an open-economy, we are very much still affected by the global situation, however it is admirable that the diversification of our economy could help reduce its impact.

(https://dollarsandsense.sg/business/what-businesses-should-know-about-singapores-economic-outlook-for-2022/)

Unemployment Rate & Job Creations

While job loss is one of the driver for property owners to potentially look at cashing out their properties, we are seeing a reduction of unemployment rate and new job creation in Singapore. (https://www.straitstimes.com/singapore/politics/54000-jobs-created-in-last-3-years-by-investments-attracted-by-edb-majority-filled-by-locals, https://stats.mom.gov.sg/Pages/Unemployment-Summary-Table.aspx) This trend is also seen in US as well – this also the US job-recession paradox which I think I will leave it to the trained economist. (https://finance.yahoo.com/news/july-jobs-report-august-5-2022-123238307.html)

High Rental Rate/Demand & Home Ownership

One other driver for distress property sale is vacate units or extremely low rental yield. In Singapore, we are seeing record rental rate across both the private and HDB with demand higher than supply in the residential segment. https://www.srx.com.sg/research/60661/condo-and-hdb-rents-increase-16-and-09-respectively-in-january-2021. The high home ownership in Singapore could also means that we might see resilient in prices especial in non-prime HDB estate or the mass market private segment where buyers/sellers are buying for own stay.

Government Intervention

While many articles focused on the cooling measures that have been introduced, these creation also provided levers for government to activate should they need to stimulate the property market. In 2018, the government reduced the Seller Stamp Duty holding period from 4 years to 3 years – that sparks the Enbloc cycle then and property prices. During the Covid pandemic, MAS also introduced the special financial relief programme for loans – we did not see a drop in property prices and surprisingly, property prices across all segments have soar to new heights. heights. https://www.moneysmart.sg/covid-19/special-financial-relief-programme-ms

CONCLUSION:

While we cannot 100% predict how the property market will be like moving forward especially with global uncertainties and tensions, what we can control is our property decision – knowing not just the potential capital gains but also the risks, trade-offs that will come along with it. Importantly, there is no right or wrong decision but an informed one that is tailored and clear for you and your family.